It’s no secret that cash is becoming extinct in 2022. After a recent study by Link found that cash payments across the UK would make up as little as 10% of all transactions in the next decade, we could be on our way to a digital cashless future.

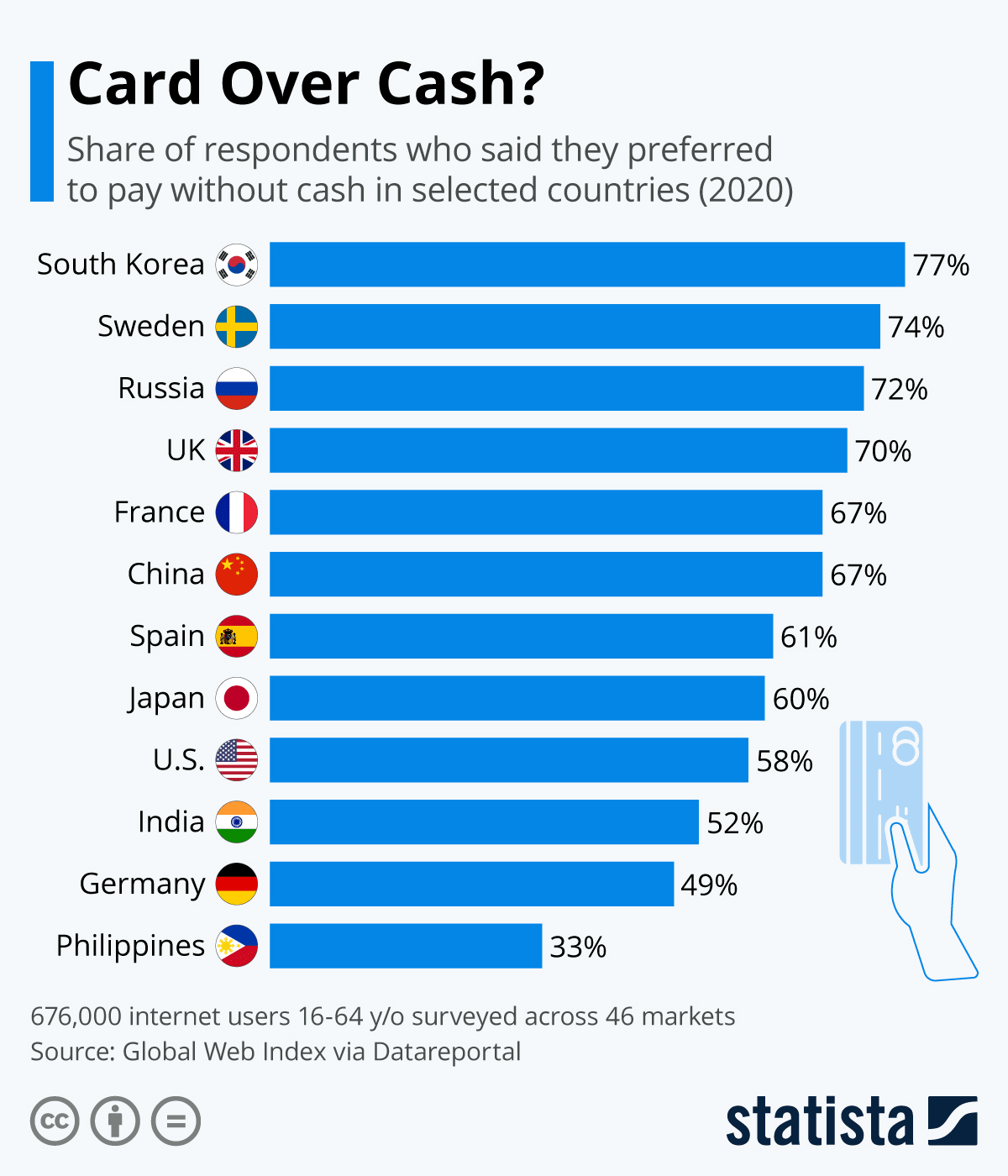

With 70% of UK-based respondents now opting to pay with a card over cash, the evolution of online banking has continued to transform how we move money in 2022. From a spike in fintech adoption to a rising interest in cryptocurrency, money management has become a data-based affair.

As we jump into a cash-free tomorrow, could big data be playing a key role in banking’s digital shift? Read on as we delve into the future of predictive payments, digital data security and AI’s impact on the financial sector.

Are We Heading Towards A Cashless Future?

59% of the global population believes that cash will disappear by 2030 according to Thoughtworks research. After Fintech proved to be the most successful evolving industry in 2021, it’s no surprise that digitally active audiences are opting for new technology-infused transactions aids such as Paypal and Monzo.

In fact, in the wake of COVID-19’s push towards an e-commerce boom, online payments soared as more consumers than ever before engaged with cross-border transactions and took steps to simplify how they exchanged money.

“Cashless transactions are rocketing and the UK has by far the largest number of payments made by card, phone or electronically in Europe, amounting to annual revenue of some €106 trillion per year,” claims Thoughwork’s Financial Director, Phil Hingley. “Some retail sectors – such as transport – are already almost entirely cashless and I see other sectors rapidly catching up. The question is, when will cash disappear from our pockets?”

As card payment stats continue to multiply, so does the use of other forms of digital transactions. Cryptocurrency adoption, for example, has taken off in a post-COVID digital arena after 97% of digital currency users confessed their confidence in the cashless currency form.

The question is, how is big data driving this gradual shift? As the mastermind behind fintech success, AI and big data-based systems are constantly influencing smart money movement and breaking barriers for instant payment apps.

“With coins extinct and paper currency on its last legs, consumers will be making instant payments from their mobile and wearable devices,” Hingley predicts. “Big data will guide our buying decisions, restocking our shelves and giving answers to the financial questions we’ve had for the last decade.”

How Will Banks Use Big Data In A Cashless Society?

Firstly, let’s have a closer look into what the term big data could really mean for the banking industry.

Defined by Investopedia, “Big data refers to the large, diverse sets of information that grow at ever-increasing rates. It encompasses the volume of information, the velocity or speed at which it is created and collected, and the variety or scope of the data points being covered (known as the “three v’s” of big data).”

Currently, the big data and analytics market is worth over $274 billion worldwide. As one of the fastest growing industries alongside financial technology and artificial intelligence, big data has had a significant impact on a number of sectors, ranging from corporate security to legal decision-making to smart finance.

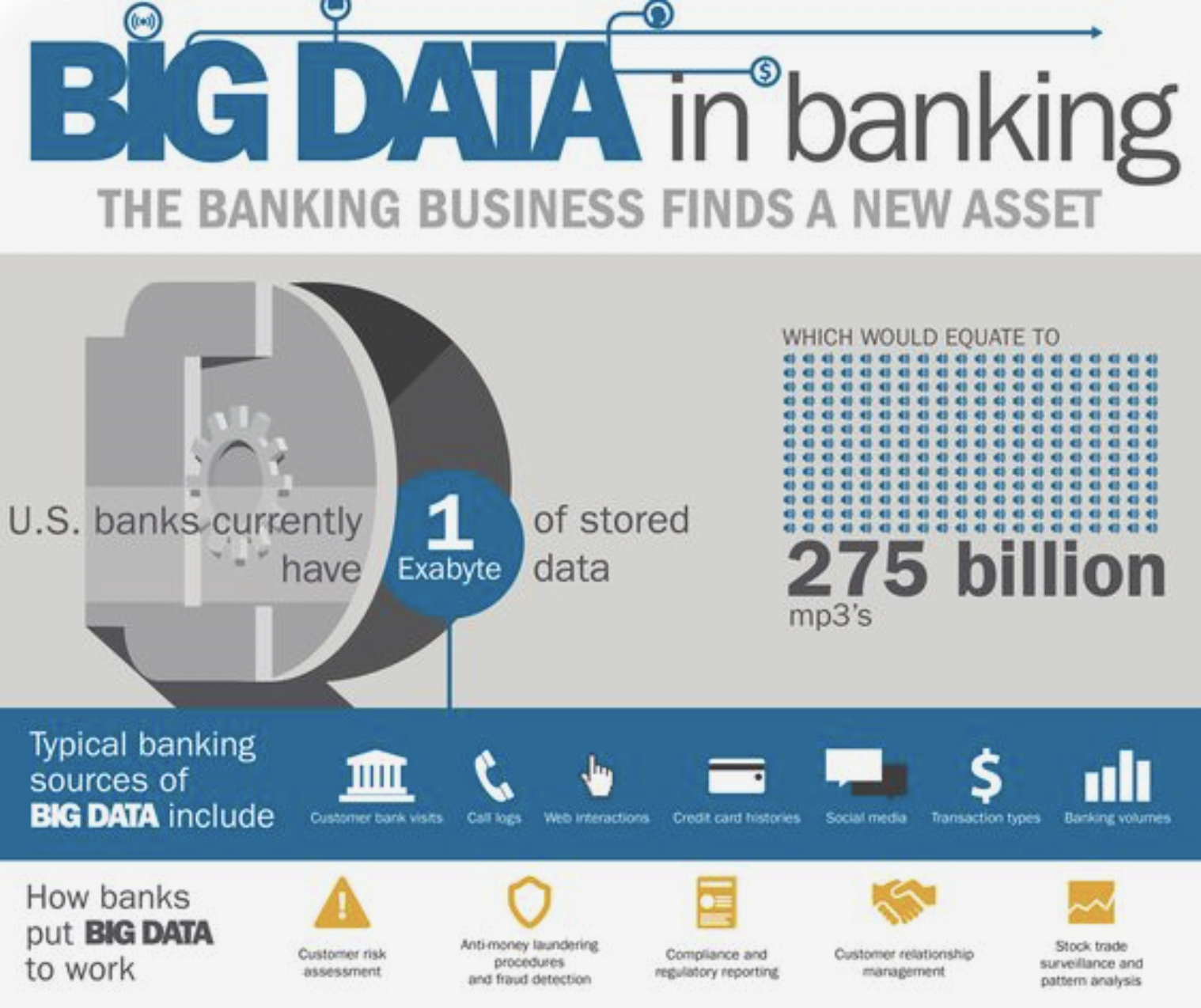

Banking institutions, in particular, have over 1 Exabyte of stored data in 2022, which is collected from call logs, web interactions, consumer histories and institution visits.

As society slips into a cashless future, traditional banking methods simply don’t cut it in 2022. With the popularity of open banking rising amongst consumers, new digital first institutions are using big data to stay ahead of high levels of online transactions, cross-border payments and a push for fintech-infused money movement.

Here are some of the current key uses of big data in the banking sector and the benefits a data-led shift could have for the financial industry:

- Data Comparison: Investing in big data analytics has provided banking institutions with a wealth of access to consumer expenditure history, incomes and transactions. With a wider range of smart analytics at hand, banks can digitally predict future transactions and use consumer data to influence credit extensions, loan handouts and mortgaging.

- Fraud Prevention: Big data science is constantly used to assess risks within the baking industry. Infusing blockchain-based cyber security, big data analysis can aid banks when processing information that requires auditing, reporting and compliance verification. This reduces the risk of consumer fraud and information-based breaches.

- Consumer Personalisation: Investing in big data enhances customer base segmentation. Using analytics, banks can divide consumers into several sectors, according to data-based indicators. With more information at hand, banks can therefore diversify their customer service and feedback, based on predictive data models.

Are There Cash Challenges Ahead?

While big data’s impact on the financial industry continues to remain positive amongst the majority, a cashless future could still pose challenges to a select few.

After a recent study found that 8 million consumers in the UK either still rely on cash payments or struggle to make a digital payment, a cashless future may pose an issue to older generations, small business vendors and disconnected consumers.